In today’s times, when a person with a regular job is unable to provide all the luxuries and needs for himself and his family, he often turns to EMIs—equated monthly installments—for help. EMI has completely changed the way people spend. Now it has become easier for people to buy a house, car or expensive electronic goods, because now there is no need to pay the full price of anything at the time of purchase. However, one important thing that everyone should keep in mind is that while EMIs are undoubtedly helpful, they also have an equally profound impact on your financial decisions—something that people often don’t fully understand.

How EMIs shape your financial life

Most importantly, when you first take a loan, the EMIs often seem manageable and reasonable. However, as you later take out more different types of loans—like a home loan, car loan or personal loan—a larger portion of your income starts going towards paying these EMIs. Gradually, your entire income is spent in paying these installments.

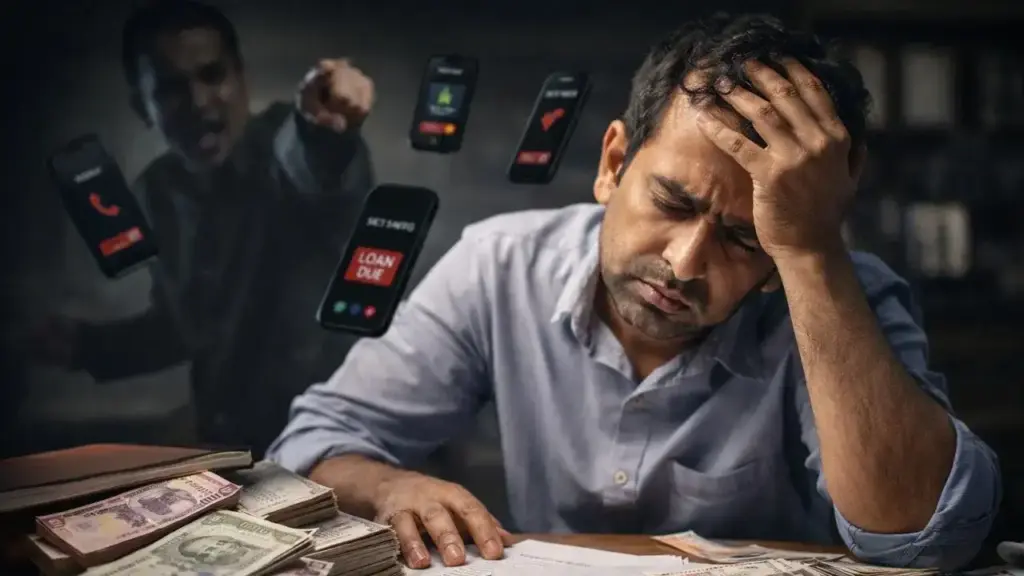

Why can taking high EMI be dangerous?

EMI is a fixed financial responsibility that you have to repay on time, every month. Any delay in payment leads to penalty and adversely affects your credit score. Also, think about the potential complications that could arise if you or a family member had a medical emergency, or your job situation changed—situations that could easily turn into a major financial crisis.

What effect does it have on your lifestyle?

Due to EMI responsibilities, you may often have to make some compromises in terms of your lifestyle. For example:

* You may have to reduce your holiday plans.

* Your personal expenses may reduce.

* Your ability to learn new skills or invest in your personal development may be hindered.

How can you strike the right balance?

Financial experts generally recommend that the total of your monthly EMI payments should not exceed a certain, pre-determined percentage of your total salary.

Before taking a loan, ask yourself these questions:

* Will I be able to repay this loan comfortably and without any stress? * Do I have enough funds for emergencies?

It is important to think about the future

It is not wise to take a loan only on the basis of your current income. It is important that you plan for the future, as there is no guarantee that your income will always increase. It is always a wise move to have a little savings.